Semi-monthly STRC Divs Will Increase Monthly STRC ATM to $10B

Originally published on X

Related Research

STRC’s new dividend cadence from monthly to semi-monthly will drive down “Time to Recover” to $100 par, and increase the frequency of ATM at par due to increased frequency of dividend arbitrage opportunities.

The binding restriction: Nasdaq Rule: minimum 10 calendar days between dividend declaration and the record date.

This move will likely dampen the volatility of STRC if for no other reason than the dividend payout per ex-div date will be half the value as paid in the monthly cadence.

Therefore, the arbitrage players who buy before the ex-dividend date and sell right after have two opportunities per month to do so.

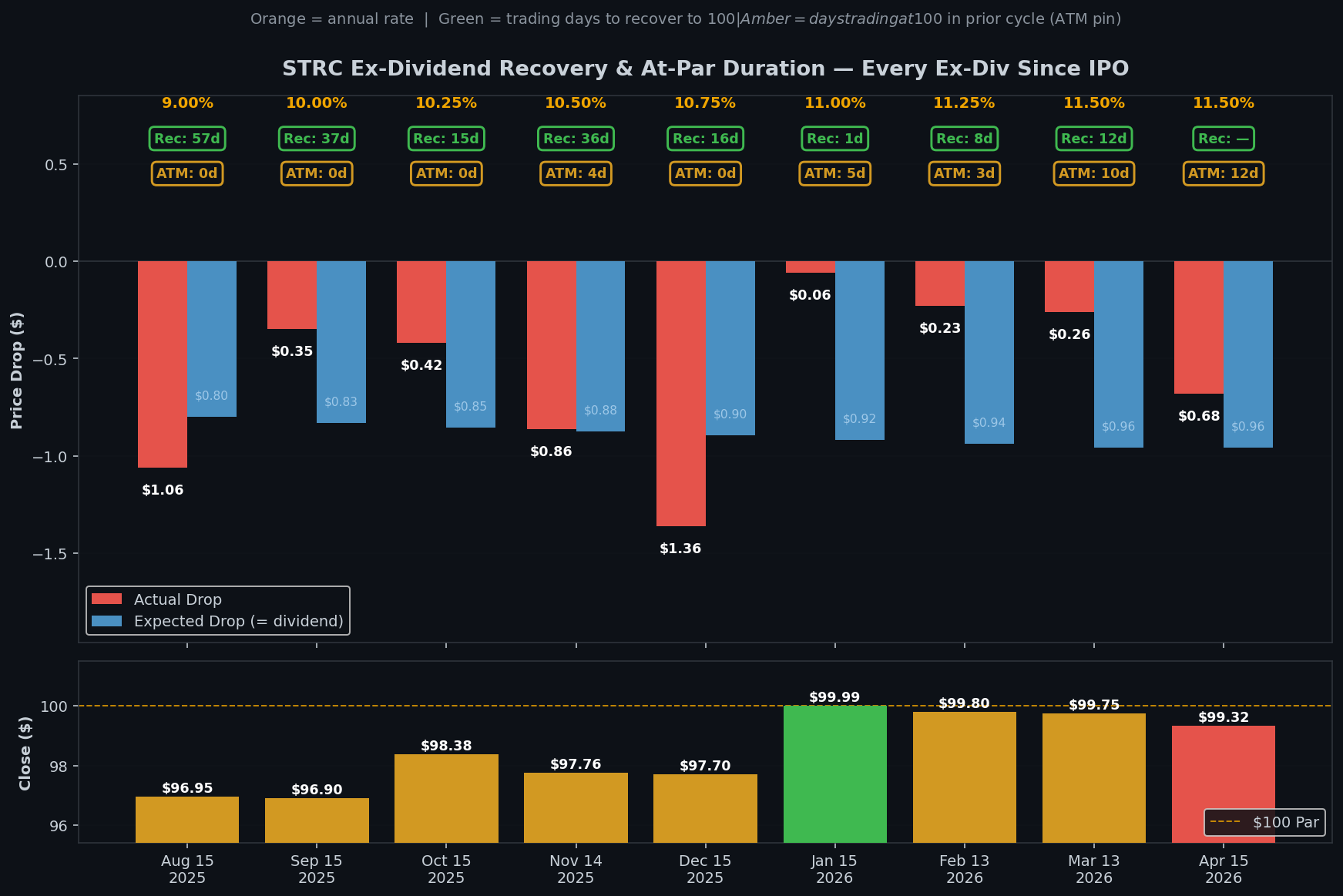

If there was no net buyers or sellers of STRC, then the price of STRC should theoretically trade down on the ex-div date by the monthly div payment. Right now, that’s about $0.95 monthly, and after the semi-monthly change, this will be $0.47 every two weeks.

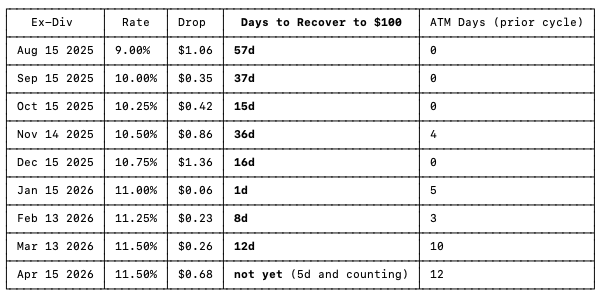

The table below shows the time to recover to $100 dollar par after each of STRC’s historical monthly dividends. Clearly the time is compressing for STRC to regain it’s peg.

With Semi-monthly cadence, time to recover will speed up dramatically. The result is that STRC will spend a larger percentage of each month at 100 dollar par.

(Mathematically it should spend the same amount of time, but I argue that a smaller gap to par will encourage faster recovery as a percentage of the time between ex dividend windows simple because the time between 99.70 and 100 has been closed much faster than 99.30-99.70. TIME TO RECOVER IS NON LINEAR.)

The next chart illustrates the drop on the monthly ex div date and the monthly div paid out. If the drop is less than the div, there exists an overnight arbitrage which feeds the ATM volume prior to each div date. Get in at 100, hold through record date, sell on ex-div date, and capture the difference between div and the drop in STRC price, for a very little hold period (low risk, high time value).

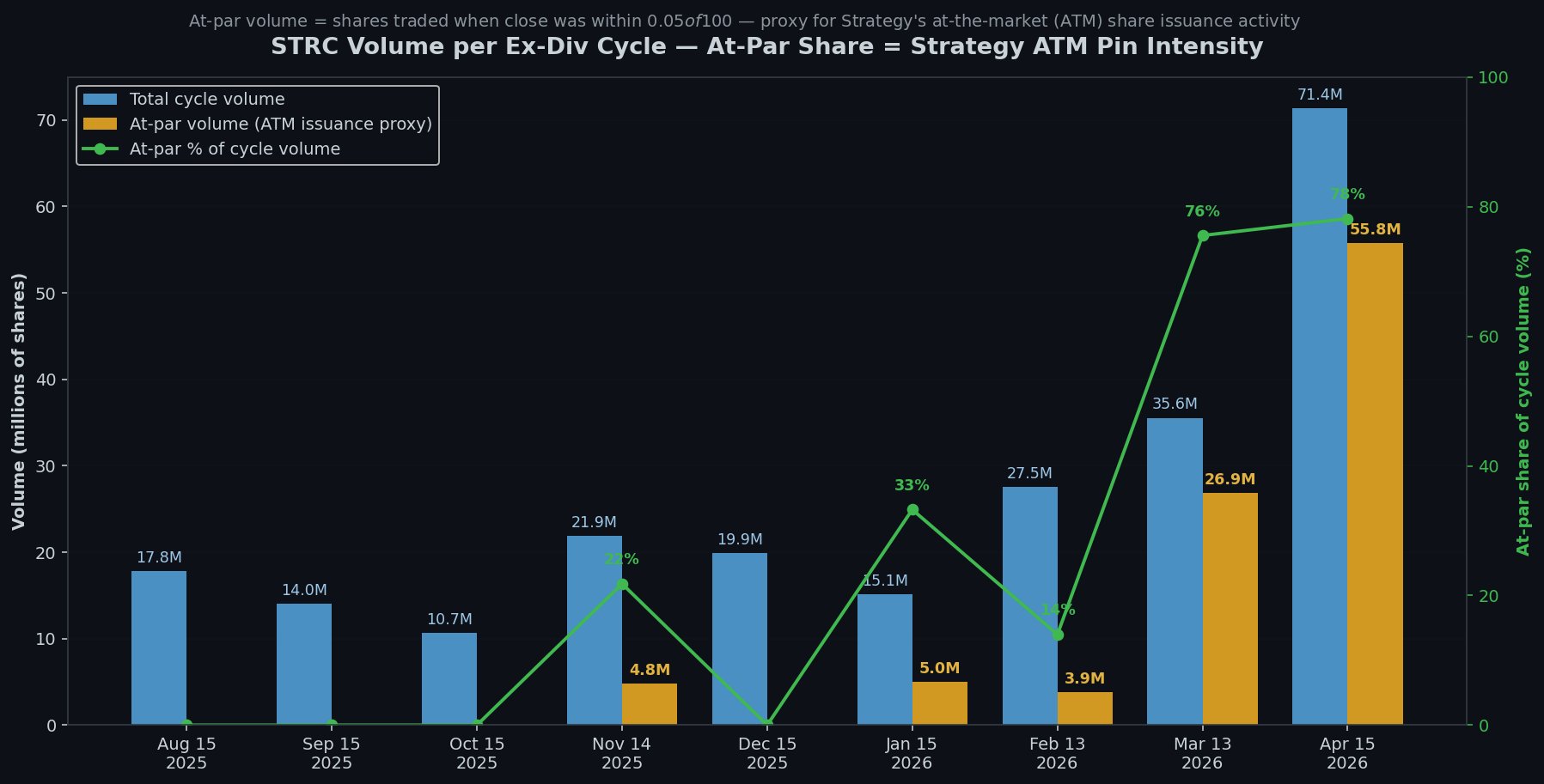

The chart below shows how the STRC volume has been ramping pre ex-div date. Therefore, with more time spent closer/at par, it is likely we could see this continued ramp in daily volume twice per month. The arbitrage traders seem to be more concerned with the time value of their money trying to capture overnight rate, then long term holding strategies.

Semi-monthly dividend cadence will likely be net positive on the issuance of STRC because arbitrage traders get two shots at an overnight div capture instead of their single monthly shot now. They are less concerned with the magnitude of the div arbitrage (which is not static), but with getting in and out; capturing whatever arb exists in the shortest amount of time.

More opportunities to arb, more volume, more ATM at par, more STRC outstanding.

Founding Member

Dan Hillery is a Founding Member of True North. He covers macro strategy, derivatives, preferred equities, and Bitcoin price modeling. Dan was profiled in the Wall Street Journal for his MicroStrategy investment thesis.

Related Research

STRC Will Become a Part of Common Investor Vocabulary

Mar 31, 2026

CommentaryStrategy Q1 2026 Earnings Call — Full Q&A Notes

May 5, 2026

AnalysisSTRK at $400 will Dominate Strategy's Trading Volume

May 1, 2026

CommentaryWeekly Signal: April 13–17, 2026

Apr 17, 2026

AnalysisBillions of Dollars backed by STRC.

Mar 13, 2026

AnalysisStrategy is Trading Bitcoin's Power Law Trend

May 19, 2026