The 2028 Intelligence Policy Response

Originally published on X

Related Research

June 30, 2028

Interest rates have now been at 0% for more than a year.

This morning, the Federal Reserve announced a new quantitative easing program totaling $1.3 trillion, focused on long-duration Treasuries, mortgage-backed securities, and targeted credit facilities tied to employment stabilization. The balance sheet will expand again. Liquidity conditions will loosen further. But where does the new liquidity ultimately go?

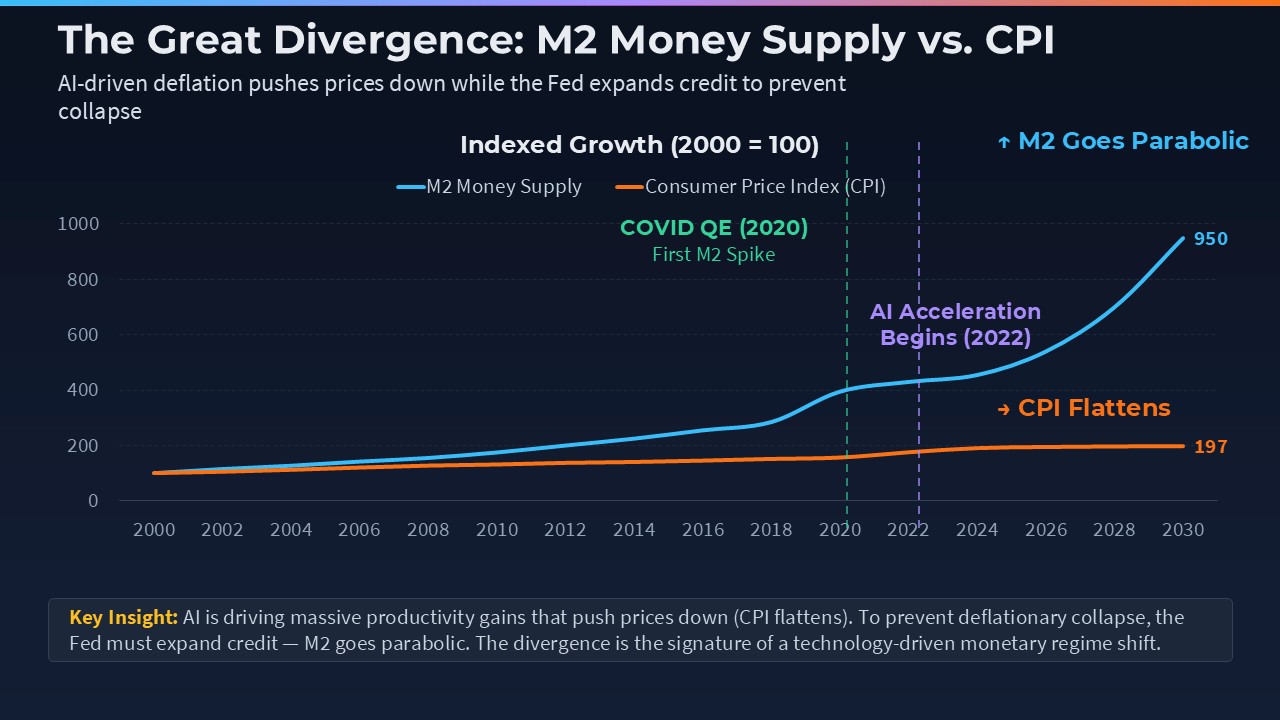

The last two years have been defined by disruption. Artificial intelligence accelerated productivity, compressed pricing power, and destabilized entire business models. White-collar employment rolled first. Consumption followed with a lag. Equity multiples compressed. Housing demand softened in income-sensitive ZIP codes.

The system bent, quickly like 2020. However, just like 2020, it did not completely break.

The defining variable of this cycle has been uncertainty around the AI policy response.

The uncertainty window

Short-term disruption of this magnitude creates a vacuum of confidence.

Investors are unsure how fast central banks will respond. They are unsure how aggressive fiscal authorities will be. They are unsure which industries will be stabilized and which will be allowed to fail.

In the early phase of the shock, that uncertainty matters more than future liquidity.

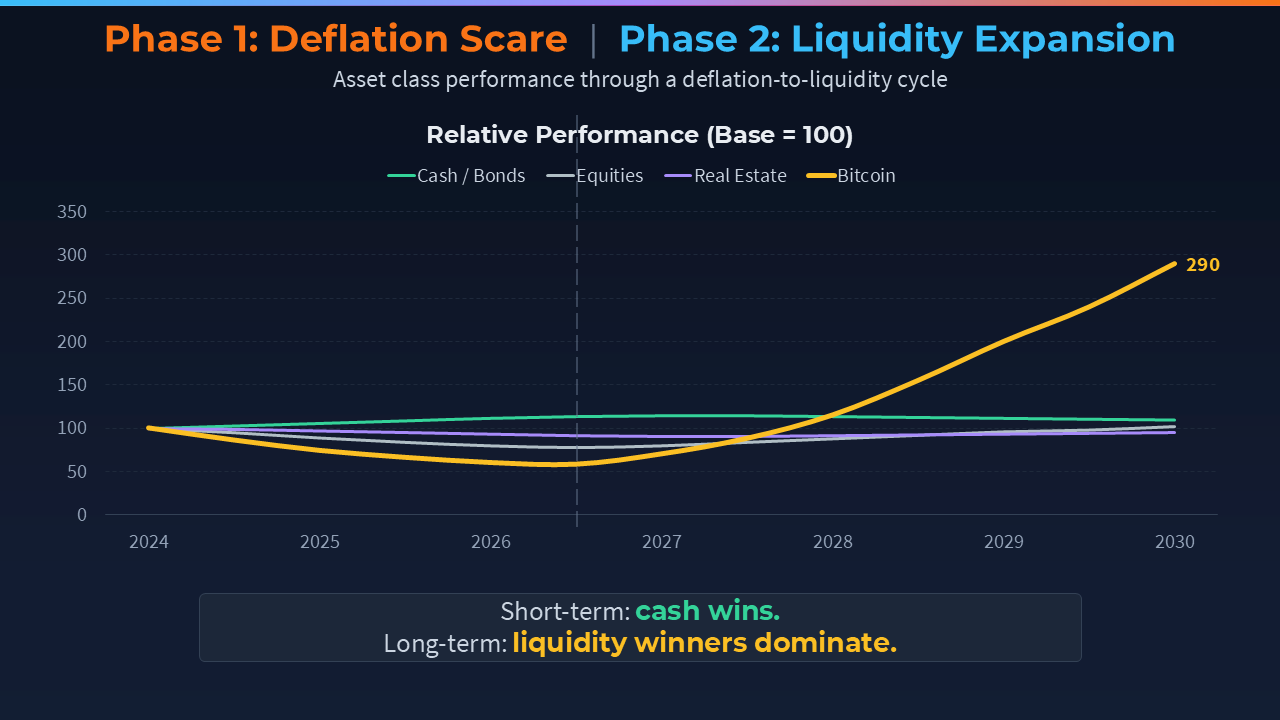

If policymakers hesitate, or if political gridlock delays fiscal expansion, the market defaults to safety. In that scenario, cash and sovereign bonds receive the only meaningful bid. Everything else sells off. Equities compress. Credit spreads widen. Real estate weakens. Bitcoin drops.

Treasuries rally aggressively. Cash becomes king. Volatility spikes across risk assets.

That phase can feel disorderly. It can feel systemic. It can resemble a broad liquidation.

However, it does NOT last.

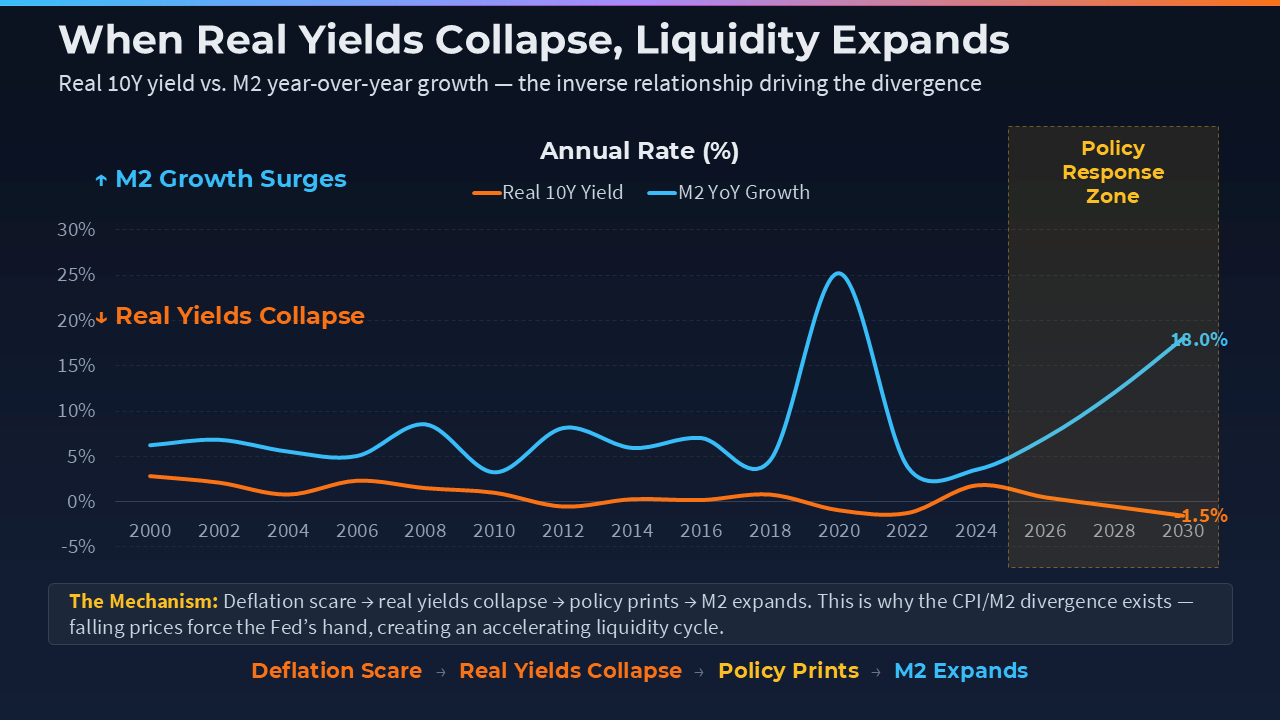

The deflation signal

An extreme bid for cash and bonds is not a sign of health. It is a signal that the market perceives rising deflationary risk.

Falling yields. Widening spreads. Weak equity performance.

Those are precisely the conditions that accelerate the central bank and government response.

The more aggressively markets price deflation, the more aggressively policymakers move to prevent it. Monetary authorities cut rates to zero. They expand balance sheets. They launch credit facilities. Fiscal authorities introduce extended unemployment benefits, pseudo-UBI, and targeted financial support.

The bid for bonds becomes the catalyst for liquidity expansion.

The uncertainty window closes once the response becomes visible.

The policy sprint

Once the response begins, it moves quickly.

Rate cuts arrive first. Liquidity facilities follow. Quantitative easing scales. Fiscal spending expands.

Policymakers act to stabilize nominal aggregates and broad market indexes even if they allow structural change in specific industries. Some sectors remain impaired. Some firms fail. Some workers never fully regain prior income levels. The government does not restore every legacy model.

It does prevent a deflationary spiral.

Broad money responds accordingly.

M2 accelerates sharply. Credit conditions ease.

The system transitions from uncertainty to ample liquidity.

Sideways indexes

Artificial intelligence continues to reshape the real economy. Productivity rises. Costs fall. Margins churn. Entire sectors reorganize.

Equities face ongoing valuation challenges as business models adjust. Real estate stabilizes without sustained real appreciation. Traditional fixed income yields little after the initial rally.

Lower rates and fiscal expansion prevent collapse. They do not restore broad-based growth across every sector.

Market indexes move sideways for extended periods. Dispersion increases. Capital and liquidity are ample but selective.

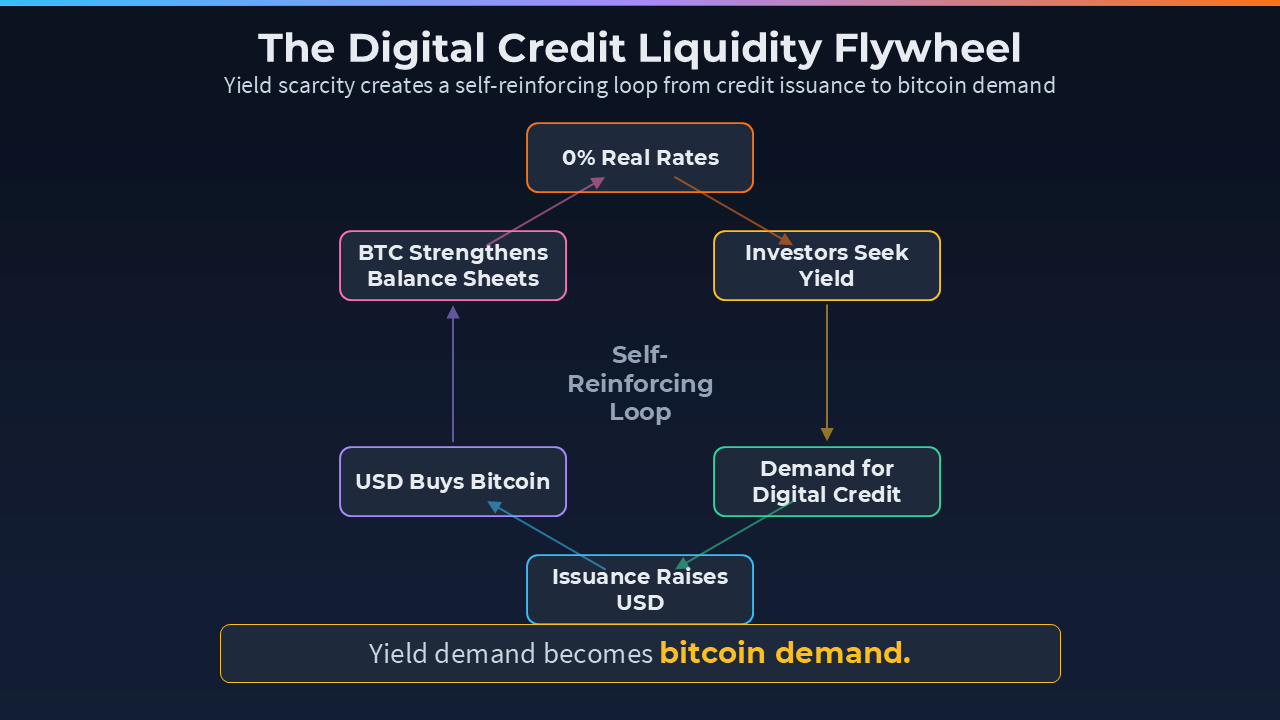

The zero-rate hierarchy

After a year at zero, investor preferences have shifted. Cash provides safety without return. Bonds provide price stability without income. Broad equities provide exposure without clarity.

Investors optimize for durability, liquidity, and yield. Assets that offer all three attract disproportionate flows. Digital credit has emerged as one of the primary beneficiaries.

Digital credit refers to publicly traded credit instruments backed by balance sheets that hold large quantities of bitcoin. Examples include STRC and SATA, liquid yield-bearing securities designed to trade near par while distributing double-digit % income. These instruments function as a new form of market-based credit, combining the stability profile of traditional preferred or structured credit with balance sheets positioned to benefit from monetary expansion. In a zero-rate world, they offer something rare: liquidity, perceived durability, and meaningful yield.

Demand intensifies as traditional fixed income yields compress.

Issuance raises dollars. Those dollars acquire bitcoin. A reflexive loop forms between USD yield demand and bitcoin accumulation.

The monetary expansion

As quantitative easing expands and fiscal deficits widen, broad money grows rapidly.

The initial deflationary impulse from AI remains visible at the micro level. Prices compress in competitive industries. Wages face structural pressure. Creative destruction accelerates.

At the macro level, monetary expansion dominates.

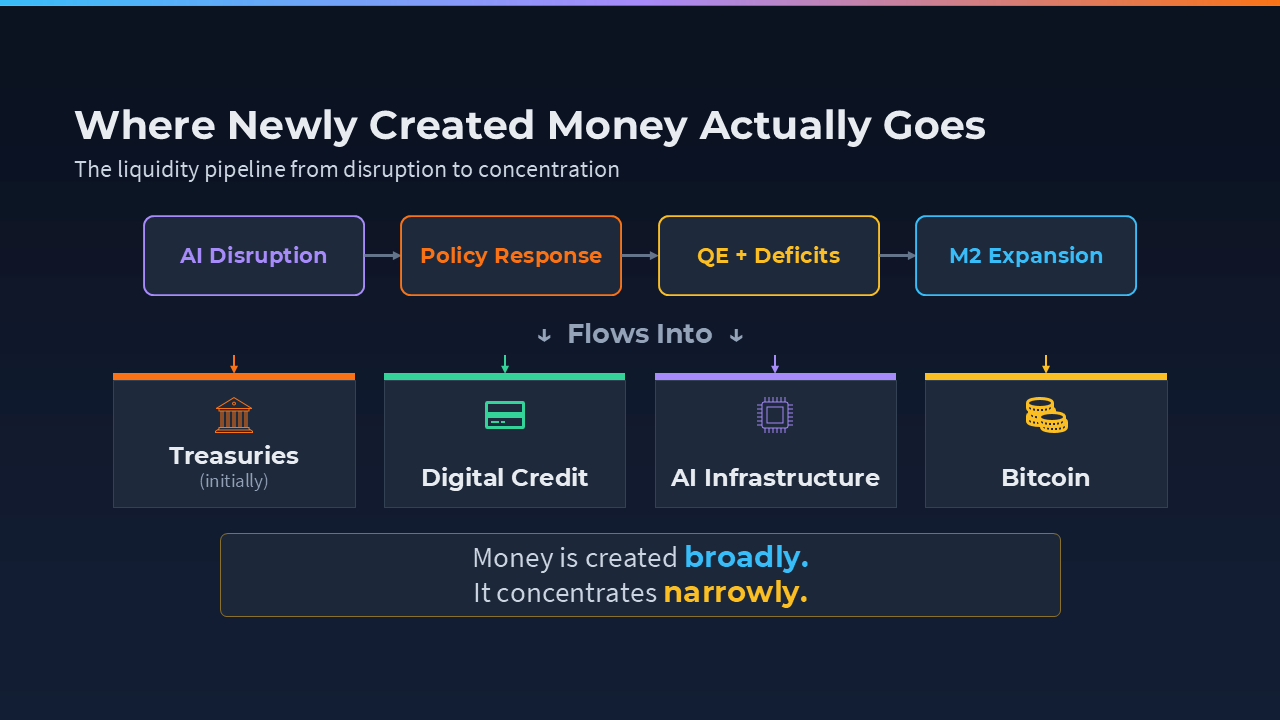

Liquidity accumulates faster than traditional assets can absorb it through earnings growth or rent appreciation. The result is divergence.

AI infrastructure continues to attract capital. Digital credit benefits from yield scarcity. Bitcoin absorbs monetary expansion directly.

Bitcoin does not depend on labor income. Bitcoin does not rely on earnings multiples. Bitcoin reflects monetary liquidity.

The timing problem

One of the defining challenges of this cycle is timing.

There are periods where cash and sovereign bonds may receive a powerful bid. During moments of acute uncertainty, capital moves toward immediate safety and liquidity. Short-duration instruments and Treasuries can outperform sharply for stretches of time. That phase can feel convincing. It can feel persistent.

The difficulty is that its duration is unknowable.

No investor knows exactly how fast central banks will move. No one knows how quickly fiscal authorities will respond once labor markets deteriorate further. The expansion of credit into AI infrastructure, digital credit markets, and bitcoin-linked balance sheets will occur. The timing of that expansion remains uncertain.

The policy response could accelerate tomorrow. It could take another year. It could arrive in waves rather than all at once.

Attempting to time that inflection precisely is nearly impossible.

Holding some liquidity during the uncertainty window is rational. USD cash reserves provide optionality. Short-duration instruments can perform well during acute deflation scares. These allocations create flexibility when volatility spikes.

Over longer horizons, however, the trajectory becomes clearer.

Rates gravitate toward zero in a deflationary shock. Monetary and fiscal responses expand the money supply. Credit eventually grows around the most productive sectors. Liquidity ultimately concentrates into assets with clean exposure to that expansion.

The end state is easier to model than the path taken to reach it.

For that reason, maintaining meaningful exposure to the assets most amplified to long-term monetary expansion remains logical even during periods of short-term uncertainty. An amplified position in those assets recognizes that the precise timing of the policy pivot cannot be known in advance, while the direction of the eventual response is far more predictable.

The transition from uncertainty to liquidity may occur suddenly. It may unfold gradually. It will likely be impossible to time perfectly.

VP of Bitcoin Strategy, Strive

Joe Burnett is VP of Bitcoin Strategy at Strive (Nasdaq: ASST) and the host of The Income Show on True North. Previously, he served as Director of Bitcoin Strategy at Semler Scientific.

Related Research

There’s a Wealth Shortage

Jun 16, 2026

CommentaryWhat Is Money Printing?

Mar 26, 2026

CommentaryWe Live in a Dissimulation

Jan 23, 2026

CommentaryThe Dual Decay

Jan 20, 2026

AnalysisBitcoin Is Missing a Central Bank. Strategy Is Building One.

Jan 26, 2026

CommentaryThe Singularity Has Begun

Jan 17, 2026